Home buyers and property investors often ask,

"Can I keep my HDB flat and buy a private property?”

"Can I afford to buy another condo?”

Often the answer depends on whether it makes sense to do that in view of financial implications. In this article, we will discuss your key considerations if you wish to own 2 properties. Thereafter, we will showcase a few case studies.

The key considerations are:

- Minimum Occupancy Period (MOP)

- Citizenship or Residency Status

- Buyer’s Stamp Duty (BSD)

- Additional Buyer’s Stamp Duty (ABSD)

- Total Debt Servicing Ratio (TDSR)

- Loan-to-Value (LTV) Ratio

- Use of CPF Funds

- Decision Chart

- Case Studies:

(A) Keep HDB flat and buy an investment condo

(B) Sell HDB flat and upgrade to a private property - Comparison Between Selling and Keeping HDB Flat

- More FAQs

1. Minimum Occupancy Period (MOP)

Whether you bought a Build-to-order (BTO) unit, a new Executive Condo (EC) or a resale flat from the open market (with or without grant), you will have to observe the MOP. During this period, there are certain restrictions. Here are some points to note:

- You cannot sell your flat within this period

- You cannot rent out the entire flat (although room rental is allowed)

- You cannot acquire another property, local or foreign

- The MOP starts from the date of key collection to your unit

- You need to physically stay in the flat; if you had rented the flat with HDB approval, it does not include the rental period.

The MOP is generally 5 years although there are a few exceptions. Take a look at the table below from HDB:

PURCHASE MODE | MOP DURATION |

Flat bought directly from HDB (includes BTO) Design, Build and Sell Scheme (DBSS) flat bought from a developer; Flat bought under SERS with Portable SERS Rehousing Benefits; Resale flat bought from open market with CPF Housing Grant; 2-room or larger flat bought from open market without CPF Housing Grant | 5 years |

Flat purchased under the Selective En bloc Redevelopment Scheme (SERS) | 5 years from date of occupation OR 7 years from date of flat selection, including wait time and occupation period; whichever is earlier |

1-room resale flat bought from open market without CPF Housing Grant | No MOP |

Executive condominium (EC) bought from a developer | 5 years. Thereafter, ECs may only be sold to Singaporeans and Permanent Citizens. After 10 years, the EC is considered privatized and may be sold to foreigners. There is no MOP for resale owners of ECs |

Video: An Introduction to HDB MOP (Minimum Occupation Period)

Watch this entertaining video about HDB MOP to find out more!

2. Citizenship & Residency Status

Only Singapore citizens are allowed to own a HDB flat and a private property at the same time. However, they are not allowed to own a private property first and then purchase a HDB flat thereafter unless they dispose of their private property.

Permanent Residents (PR) are not allowed to buy a condo if they own a HDB flat. If they buy a condo (completed or under construction), they are required to dispose of their HDB flats within six months.

3. Buyer’s Stamp Duty (BSD)

Buyer’s Stamp Duty (BSD) is computed based on the purchase price or market value of the property, whichever is higher. All residential and non-residential properties will be subject to BSD in transfer or sale and purchase transactions.

The rates as illustrated in the table from IRAS:

A quick formula for Buyer Stamp Duty (BSD) is shown below:

Residential Properties:

- Below $1M: Purchase Price x 3% LESS $5,400

- Above $1M: Purchase Price x 4% LESS $15,400

Commercial Properties:

- Purchase Price x 3% LESS $5,400

Example:

For a $1 million private condo, your BSD will be $24,600. Here’s the calculation:

$1,800 (for the first $180,000)

+ $3,600 (for the next $180,000)

+ $19,200 (for the next $640,000)

= $24,600

Read More >> Buyer's Stamp Duty (BSD)

Click to read this post explaining Buyer's Stamp Duty (BSD) in detail.

4. Additional Buyer's Stamp Duty (ABSD)

The ABSD applies to purchases of more than one residential property (i.e. 2nd property, 3rd property etc). The ABSD is payable in addition to the BSD.

Since December 2011, the ABSD was introduced as a cooling measure to moderate the demand for investment properties by both Singaporean and foreign buyers.

- Singapore Citizens are subject to an ABSD of 12% for the 2nd property purchase, and 15% for the 3rd and subsequent property purchases.

- Permanent Residents (PR) are subject to an ABSD of 5% for the 1st property purchase, 15% for the 2nd and subsequent property purchases.

- Foreigners are subject to an ABSD of 20% for all property purchases.

- Entities are subject to an ABSD of 25% for all property purchases.

Some exceptions to the rules apply:

- The first marital home between a Foreigner and Singapore Citizen is exempt from ABSD. (See Below)

- Nationals and Permanent Residents of Iceland, Liechtenstein, Norway or Switzerland, and Nationals of the United States of America will be accorded the same Stamp Duty treatment as Singapore Citizens.

ABSD Remission for a married couple

A married couple may be eligible for ABSD remission on the purchase of a residential property if the remission conditions under the Stamp Duties (Spouses) (Remission of ABSD) Rules are met.

For more information, please click here which will lead you to IRAS’ website.

Example:

If you are a Singapore Citizen who currently owns a HDB flat and want to purchase a private property at $1million, you will need to pay an additional 12% ($120,000) above the BSD. Since your property count is now TWO, if you should wish to purchase yet a 3rd condo at $1 million, you will have to pay an additional 15% ($150,000) above the BSD.

If a home owner is thinking of upgrading from a HDB to a private property and subsequently purchases a second investment property, there are ways to structure such that ABSD can be minimized.

If you want to find out more, contact Property Science consultants now.

Read More >> Additional Buyer's Stamp Duty (ABSD)

Click to read this post explaining Additional Buyer's Stamp Duty (ABSD) in detail.

5. Total Debt Servicing Ratio (TDSR)

The TDSR was introduced in 2013 by The Monetary Authority of Singapore to encourage prudent use of loans to finance the purchase of a property.

The TDSR is the sum of your total liabilities divided by your gross monthly income.

It limits the home loan quantum by ensuring your monthly repayments for all your outstanding debts – existing mortgage, credit cards, car loans, student loans, personal loans, and even your salon packages and so on – do not exceed 60 per cent of your monthly income.

If your family’s combined income is $10,000 a month, the TDSR is $6000. If your total loan liabilities are $4000, this means your maximum monthly loan repayment is $2000 ($6000 – $4000).

The loan tenure is calculated using the income-weighted age of all borrowers.

If you are unsure about your TDSR calculation, contact your mortgage specialist or speak to Property Science consultants now.

Read More >> Total Debt Servicing Ratio (TDSR)

Click to read this post explaining Total Debt Servicing Ratio (TDSR) in detail.

6. Loan-to-Value (LTV) Ratio

Your loan to value (LTV) is the housing loan quantum a bank is willing to loan you based on the valuation of your property.

For your first private property, the LTV is:

- up to age 65: 75% LTV < 30 years tenure

- up to age 75: 55% LTV >30 years tenure

For your second private property, the LTV for a bank loan is:

- up to age 65: 45% LTV < 30 years tenure

- up to age 75: 25% LTV >30 years tenure

Note: For HDB flats, the tenure is maximum 25 years instead of 30 years.

For other permutations or 3rd property, consult our Property Science consultants.

DOWNPAYMENT FOR MULTIPLE LOANS

Assuming that you are able to secure a loan for your property purchase, you will have to fork out the remainder in cash and/or CPF Ordinary Account. Below are the portions that must be paid in cash (not CPF):

- 1st property loan: 5% cash

- 2nd property loan: 25% cash

The percentage is based on the purchase price, or valuation of the property, whichever is lower.

If you have cleared your first housing loan in full, you can consider yourself as taking your FIRST property loan.

Example:

Mr Lee owns a HDB flat which he is currently servicing the mortgage for and would like to purchase a condo at $1 million.

Since it is his second housing loan, he will be subject to an LTV of either 45% or 25%.

- If he wants to loan up to age 65, he needs to pay $550,000 (55%) in cash and/or CPF. Out of this, 25% must be in upfront cash.

- If he can wishes to loan up to age 75, he needs to pay $750,000 (75%) in cash and/or CPF. Out of this, 25% must be in upfront cash.

Refer to the table below for a quick summary:

Read More >> Loan-to-Value (LTV) Ratio

Click to read this post explaining Loan-to-Value (LTV) Ratio in detail.

7. Use of CPF Funds

If you are utilizing your Central Provident Fund (CPF) to fund the purchase of your second property, here are a few considerations:

(1) You may use CPF Ordinary Account (OA) to pay up to 100% of the Valuation Limit – the property price or valuation, whichever is lower. Note that you can use up to 120% of the Valuation Limit for the FIRST property.

Example: Assuming you are eyeing a condo that is valued at $1,500,000 but you purchased it for $1,400,000. Your Valuation Limit is $1,400,000 being the lower of the two. Therefore, you may withdraw up to $1,400,000 from your CPF OA.

(2) Under the Multiple Property Rule: if you have used your CPF for an existing property, you would need to set aside the Basic Retirement Sum (BRS) before you can use the excess savings in your Ordinary Account (OA) for subsequent properties. Your Basic Retirement Sum includes amounts in your Ordinary Account, Special account, investments, and Retirement Account (for over 55 years of age). For 2021, the sum is $93,000. This figure increases every year. To get more information about the BRS, click HERE.

Example: Mr Ng turns 55 years old in 2021. His BRS is $93,000. If the total amount in his CPF (Ordinary Account + Special Account + Retirement Account) is $100,000, then he may utilize $100,000 – $93,000 = $7,000 from his CPF OA account to buy the second property.

(3) To use the BRS, you need to make sure the property you are buying, or the other property (HDB) bought using CPF can cover you till age 95. If you do not have a property that covers you till age 95, you will need to set aside the Full Retirement Sum (twice the BRS) before you can use the excess OA funds to buy other properties.

(4) How much CPF you may use also depends on the age of the youngest owner. The remaining lease of the property must cover the youngest owner up to age 95. If this condition is not met, the CPF amount allowable for use will be pro-rated. You can find out how much you can use from this CPF USAGE CALCULATOR.

The CPF regulations are to ensure there is a roof over our heads in our old age but this limits the amount we can withdraw for property purchase and hence, be prepared to fork out a hefty portion of the price in cash.

Read More >> Using CPF Funds for Property Purchase

Click to read this post about Using CPF Funds for Property Purchase.

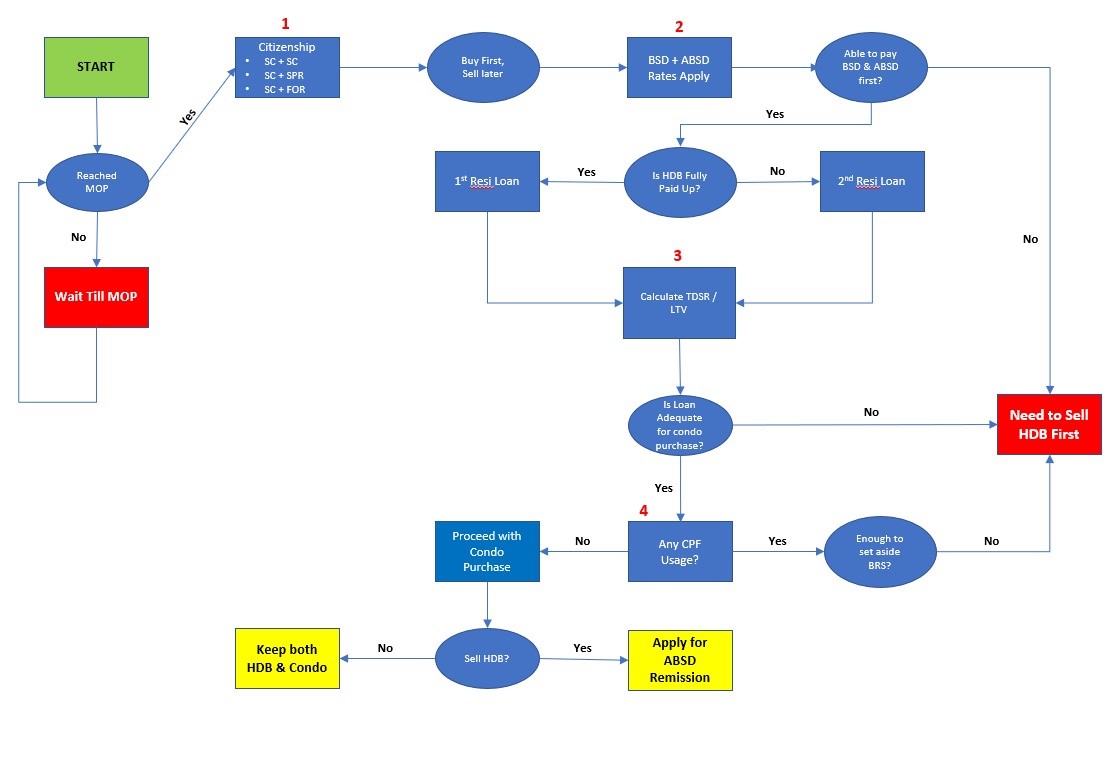

8. Decision Chart

In the chart below, we illustrate the processes and steps HDB owners have to take in order to decide what is the best decision moving forward:

If you would like us to take you through the decision chart, contact the Property Science Consultants for a no-obligation presentation.

9. Case Studies

Let’s take the example of John and Jane, both 40 years old, married Singapore citizens. (Do bear in mind that the higher ABSD applies to the second property if you are either PR or a foreigner.)

John and Jane own a 5-room HDB flat in Punggol which is about 9 years old and valued at $620,000. Their flat’s balance lease of 90 years is enough to cover them up to age 95. This means they can use their CPF OA funds to buy the next property at 100% of the valuation limit after setting aside the Basic Retirement Sum.

They took out a 20-year bank loan for $375,000 when they bought the flat from HDB which they are currently servicing.

OPTION 1: TAKE UP A BANK LOAN FOR THE NEW PURCHASE

If they wish to buy a condo at $1 million with a bank loan, below is the financial breakdown of such transaction:

- Downpayment 55% (LTV for second property is 45%) = $550,000

[Minimum cash payment 25% = min $200,000]

[CPF OA: max CPF usage if you are able to set aside the BRS = max $350,000] - Buyer’s Stamp Duty (BSD) = $24,600

Additional Buyer’s Stamp Duty (ABSD): second property rate for Singapore citizens is 12% = $120,000

- TOTAL = $694,600

- Downpayment 55% (LTV for second property is 45%) = $550,000

For this option, there is a high upfront amount of about $700,000. Bear in mind that if a loan is taken for the 45% of purchase price, the couple has to service BOTH mortgage loans for their flat and new condo.

The above case study assumes that your Total Debt Servicing Ratio (TDSR) is adequate to approve the new loan while servicing the HDB loan at the same time.

OPTION 2: CLEAR THE FIRST LOAN AND TAKE UP A LOAN FOR THE NEW PURCHASE

To minimize the upfront cash, you can choose to pay up the remaining HDB loan. This will allow you to borrow from the bank on a 75% LTV basis (rather than 55% LTV for the second housing loan).

- Downpayment 25% (LTV for first property is 75%) = $250,000

[Minimum cash payment 5% = min $50,000]

[CPF OA: max CPF usage if you are able to set aside the BRS = max $350,000] - Buyer’s Stamp Duty (BSD) = $24,600

Additional Buyer’s Stamp Duty (ABSD): second property rate for Singapore citizens is 12% = $120,000

- TOTAL = $394,600

- Downpayment 25% (LTV for first property is 75%) = $250,000

Unless you are prepared to use a lot of savings for the cash component, Option 2 at under $400,000 is more palatable.

If you choose to buy first, the 2 options in Case Study A applies.

However, if you sell your HDB flat within 6 months, you are eligible for an ABSD remission. You will have to pay up the ABSD first and get the refund later. So in terms of cash outlay, it will be rather challenging. You will be required to purchase the next property under joint ownership to be eligible for this remission.

Find out more at CPF website.

With this scenario, there are a few considerations:

- You may buy the next property under single ownership if your TDSR allows so as to allow asset planning for your future purchases. Some may even purchase 2 units (one for own use and one for rental investment).

- If you are able to plan the timeline for your next resale property, you may be able to move in seamlessly by getting an extension of stay for your flat and an early handover for your new home to facilitate renovations. This timeline management is tricky so it is best to consult a professional.

- If you are buying a new launch under construction, you may need to rent for the time being.

- You will be able to withdraw up to 120% of the Valuation Limit of your CPF for this new property. However the withdrawal limits based on the condo’s remaining lease still applies. (See section 7, Usage of CPF.)

It is best to calculate your HDB sale proceeds so that you may plan properly for your next move. Your proceeds can be derived after deducting these costs from your sale price:

- Outstanding bank loan

- Legal fees (ranges from a few hundred if you use HDB’s conveyancing service or a few thousand for private lawyers)

- Return of the CPF OA funds used and accrued CPF interest into your Ordinary Account (although this can be used for the next purchase)

- Property agent commission for the sale of your flat (typically 2% for HDB flat sale)

- Other miscellaneous cost will include HDB resale application fee, pro-rated property tax and conservancy fees, which are mostly insignificant

To buy any property, AFFORDABILITY is always the first consideration. Below is a list of factors that you need to consider in your purchase:

TOTAL FUNDS:

CPF OA funds

HDB sale cash proceeds

Cash savings

Maximum loan/Total Debt Servicing Ratio (TDSR)

TOTAL COSTS:

Buyer’s Stamp Duty (BSD)

Additional Buyer’s Stamp Duty (ABSD) (if applicable)

Legal costs

Everybody’s situation is unique, so if you would like to consider an upgrade in your asset and need a detailed financial calculation, contact Property Science.

10. Comparison Between Selling and Keeping HDB Flat

SELL THE HDB | KEEP THE HDB | |

CPF | Can use up to 120% of Valuation Limit | Can use up to 100% of the Valuation Limit |

Basic Retirement Sum (BRS) | Does not need to be set aside if you’re below 55 years old | Needs to be set aside even if you’re below 55 years old |

Bank Loan | Maximum of 75% LTV (Loan-To-Value) | Maximum of 45% LTV (Loan-To-Value) assuming there is a HDB loan |

Downpayment | Minimum 25% in cash and CPF | Minimum 55% in cash and CPF, assuming there is a HDB loan |

Monthly Mortgage Repayment | Only service one loan | Service 2 loans assuming HDB loan is still outstanding |

Additional Buyer's Stamp Duty (ABSD) | 0% | 12% |

Property Tax | Taxed on Owner-Occupied Rates | Taxed on both Owner-Occupied and Non-Owner-Occupied Rates |

11. More FAQs

Can I Buy a Condo if I Own a HDB?

Only Singapore Citizens can keep their HDB and buy a private property. However, ABSD is applicable.

Permanent Residents will have to dispose of their HDB flat, which they can only do so after the 5-year Minimum Occupation Period.

Can I Buy a HDB Flat If I Own a Condo/Landed Property?

No. You will not be eligible to buy a HDB flat as they are meant to meet basic housing needs.

Can I Buy a HDB Flat After Selling My Condo?

Yes, if you are Singaporean, you may buy a resale HDB flat.

However, if you will be required to dispose of your condo within 6 months of your HDB flat key collection. You will not be eligible to any housing grant or for the loan by HDB.

Can I Buy a BTO HDB Flat After Selling My Condo?

Yes you may do so only 30 months after the sale of your property. The same applies if you are taking a grant to buy a flat from the open market.

Can I Rent Out My HDB and Stay in a Condo?

Yes. For HDB you can only out the whole flat after the 5-year Minimum Occupation Period (MOP). However, you may rent out rooms in the flat within the MOP period. In any case, you may only buy a condo after the MOP is over.

We’re here to help you on your real estate journey.

Contact us using the form on this page and our Consultant will be in touch with you very soon.

Or contact us by phone/email.

Call: (+65) 8363 2331 / 8778 8778

WhatsApp: Glynis Tan / Benjamin Yeo

Email: findout@property-science.com