If you are buying a Housing Development Board (HDB) flat, you can either opt for a bank loan or a loan from HDB.

To assess your eligibility for a HDB loan, you may click HERE.

But before you go, read this!

How Do Bank Loans Work?

If you are taking your first housing loan, you will be eligible for a maximum of 75% Loan-To-Value (LTV) loan. The current bank loan packages (2021) offer interest rates ranging from 1% to 2% per annum. (See below for the historical bank rates.)

How Do HDB Loans Work?

If you apply for a HDB loan, you can get a maximum of 90% LTV. HDB charges you 2.6% interest per annum.

Let's work out an example:

Let’s assume that you are purchasing a HDB flat worth $500,000 valuation and taking a loan of 20 years.

With a bank loan, you will get 75% LTV. Hence, the loan amount is $375,000. At 1.5%, your total interest is $59,291 and your total repayment is $434,291. At 2.6%, your total interest is $106,309 and your total repayment is $481,309.

If you are getting a HDB loan, the LTV will be 90%. At 2.6%, your total interest is $127,571 and your total repayment is $577,571.

What implications does this have for you?

The difference in total interest between a bank loan and a HDB loan is a whopping $21,262 to $68,280!

Why is this so? While HDB gives you a 90% loan, you also pay a premium for that loan. This could result in a negative transaction for your HDB flat because your sale price may not result in enough profit to cover the difference.

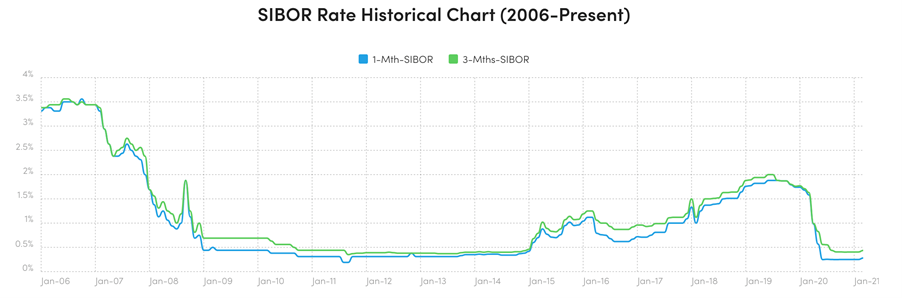

Bank Rates Over The Years

Obviously, we recognise that rates fluctuate over the years and therefore we assumed a fixed rate. We would like to share the historical SIBOR rates below for your reference:

We use the SIBOR rate as a gauge because it is the most transparent. If you were to study it, since 2006, there was only once (2006-07) that interest rates went over the 2% mark.

Of course, while historical data is no indicator of future performance, in view of the current economic situation in 2021, rates are expected to remain low.

If you would like to read more about how these rates affect your loan, and some expectations of future rates, you may click HERE.

If you are thinking of taking up either a HDB loan or bank loan, remember to consider your financial situation carefully and speak to a professional/mortgage specialist before committing to either package. Other considerations may include non-tangible factors such as HDB’s leniency when a borrower falls on hard times.

If you have further questions, wish to purchase or sell your flat, feel free to approach us HERE. We would be happy to have a chat with you.