Decoding Real Estate

Let us look at a condo that has recently obtained its TOP not too long ago to see what real estate investments can do for you when done right.

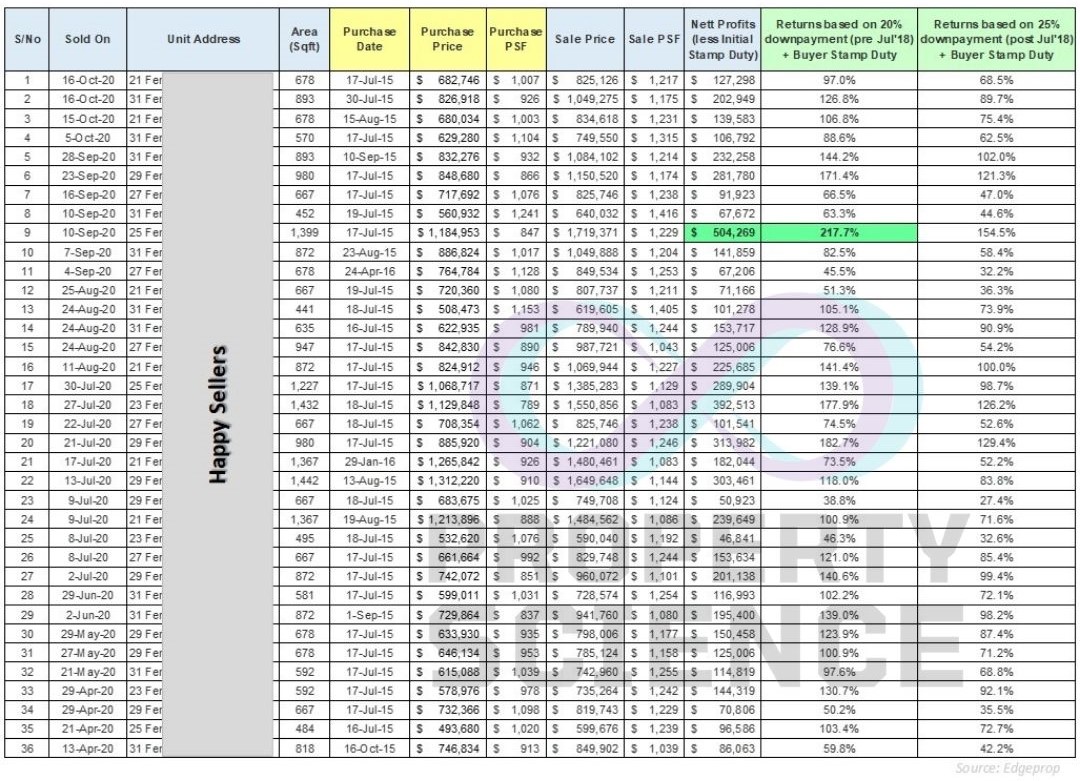

This transaction chart below shows how much the buyers who bought into North Park Residences (new launch) in 2015 and subsequently sold in 2019/2020 made.

In total, there were 183 profitable transactions to date.

The transaction data above shows that the lowest realised profit is $36,213 while the highest realised profit is $504,269. The average profit works out to $162,421 after deducting stamp duty.

Assuming the buyers took the maximum allowed mortgage loan, the highest achieved percentage return on investment based on the down payment paid is 217.7%.

All these was achieved within a 4 to 5 years’ time frame. Are you able to realistically save so much money from just your monthly income alone?

Investing in real estate is a stable and safe way towards financial freedom. This explains why all over the world, people love to accumulate properties. Unfortunately, for the layman, it is not easy to master the property market without in-depth research. Our education system does not teach leveraging on real estate as a subject.

If you want an unfair advantage, get a head start! Plan and execute your real estate moves in advance!

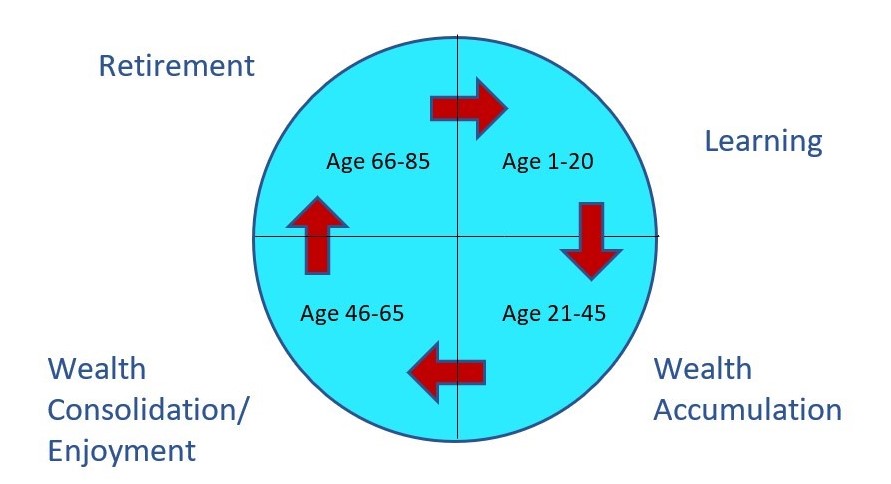

To briefly explain the chart above, each quadrant represents a life stage. There are 4 life stages: learning, wealth accumulation, wealth consolidation & enjoyment and retirement.

Our working lives are usually between age 21 to 65. During this time, many will buy their first property, which could be a HDB flat (very affordable) or a private property (with some help from loved ones).

After several years of Wealth Accumulation, some will enter Wealth Consolidation, where they are able to either upgrade their asset or purchase a second property. Many will stop their journey here.

Those who have been taught the Asset Progression Theory will proactively seek out opportunities in the market in order to upgrade their properties.

Just like us, properties also have their life cycles which see their value hitting an optimal level before they start declining. Those who are in the know will seek to offload their units before their prices stagnant or decline.

Upgrading does not necessarily mean forking out a lot of savings to buy a larger (and more pricey) property. It involves UNLOCKING the CASH that is locked up in a property by selling it, and using the money to invest in a high-performing property that will give higher capital gains or rent.

At Retirement, when kids have left the nest, some may choose to downgrade and sell off one or two assets and free up their money for their golden years.

Unfortunately, we have come across individuals who only come to realise at this point that selling their properties will result in a negative sale (where they will lose instead of gain money). For many HDB owners and some condo owners, the2.5% CPF accrued interest that has to be returned to their accounts means there is not enough left after the sale.

The million-dollar question is: Do you know what to do during each life stage? Has anyone taught you how to maximize your financial status through property? Did anyone discuss the implications of Asset Progression Theory and the consequence of missing the boat?