Decoupling involves one spouse legally giving up his or her co-owner status to become an authorised occupier.

Legally speaking, decoupling is known as a part-share transaction involving real estate; in Singapore’s context, this is usually always talking about residential real estate where hefty Additional Buyer’s Stamp Duty (ABSD) applies for 2nd and subsequent purchase of residential properties.

Decoupling happens when one partner’s share in a property is transferred to the other person. This results in a sole owner, leaving the other partner free to buy another home without having to pay the ABSD as that purchase will be seen as his or her first. The savings can be substantial.

Since the tax was introduced in 2011, many property investors and owners have used this strategy to manage the amount of ABSD they have to pay. It was really in January 2013 that this strategy became more widespread as ABSD was also applicable to second properties (instead of the third), the latest cooling measure to control the continual rise of property prices.

With the current tax regime, this means that a Singaporean buying a second home is levied an ABSD of 12%, while permanent residents (PRs) pay 15%. If the unit is a third property, the ABSD goes up to 15% for Singaporeans but stays at 15% for PRs. Read more here.

Some Things to Note When Considering Decoupling

Transferring a half share to one of the co-owners is still subject to the standard stamp duty rate of 3% to 4%, as it is considered one transaction. ABSD is also payable on the value of the share transferred if the party that is taking over the half share has more than one property.

In some cases, Seller’s Stamp Duty (SSD) may be payable if the property was purchased less than three years ago. The amount is 12% of the price on the first year, 8% on the second year, and 4% on the third year. There’s no SSD payable after that so most couples will hold on to the property for at least three full years before decoupling.

Legal fees can range from $5,600 to $6,500 as it is considered 2 transactions – one representing the party ‘transferring’ the half share of the residential property to the other party, and another representing the party receiving the half share of the residential property. A larger conveyancing firm will be able to handle the whole process.

If there is an outstanding home loan, then this must be discharged and a new mortgage obtained from the bank for the party who is taking over the share.

Check whether you incur any penalty for redeeming the loan and the cost of getting a fresh mortgage. In addition, consider if the salary of the sole owner can support the fresh loan.

If the Central Provident Fund (CPF) Board funds are involved, you must consider the refund of CPF monies to be made to the party ‘selling’ the property.

The CPF Board requires all property sellers to return the amount used from CPF with accrued interest when you sell the property. In some cases, there could be zero cash proceeds. Therefore, it is important to take note of this amount. You may log in to your CPF account using your Singpass to check the amount you owe.

For example, after you ‘sell’ your share of the property to your spouse, let’s assume you’re required to return $210,000 to CPF. However, the proceeds only come to around $190,000. This shortfall of $20,000 may not require a top up from you in cash if you sold at (or above) valuation but it means all the cash is going back into your CPF.

In order to buy your next property, you will need to pay at least 5% of the price in cash. If all the funds are locked up in your CPF, you may not have the upfront cash. We recommend careful financial calculations to achieve this. If you need advice, feel free to approach us HERE.

Other Considerations

With decoupling, there may arise the issue of trust. If there is a great disparity in value between the two properties the couple owns, there may be a dispute between who owns the landed property and who will take on the tiny investment unit, for example. When it comes to legacy planning, there may be more complications.

Some buyers have asked if there is a difference between a gift and a sale when it comes to transferring the property between one partner to the other. Do take note that Buyer’s Stamp Duty is the same for both gift and sale. The main difference is that, in the case of a sale, an actual cash transfer must take place; if it is a gift, there will be restrictions on selling the property for a few years.

Can HDB be Decoupled?

In the past, Housing Board flat owners exploited the decoupling loophole by transferring their flat to a spouse or immediate family member. They then went on to buy a private property as a first property, thus avoiding the ABSD.

Since 1 April 2016, this loophole has been closed. HDB owners are only allowed to transfer their ownership to a family member only under special circumstances such as on grounds of marriage, divorce, death of an owner, financial hardship, renunciation of citizenship and medical reasons.

Some examples of these situations would be HDB owners who have trouble servicing the mortgage and have family members who are willing to take over the lease. The chronically-ill also may get an exemption to bequeath the flat before their illness worsens. All other cases will be reviewed and approved on a case-by-case basis.

CASE STUDIES

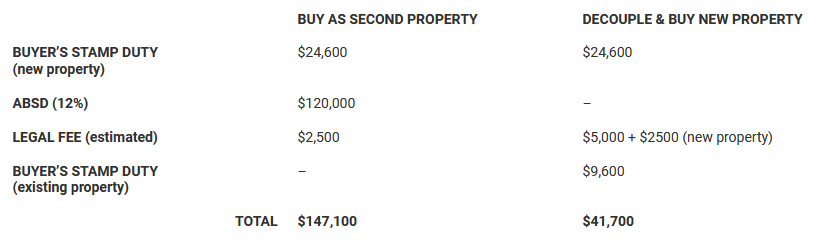

SCENARIO 1: WHEN DECOUPLING RESULTS IN SAVINGS

John and Jeannette bought their first apartment together. After the three years Seller’s Stamp Duty period was over, they had their eye on an investment property that cost $1 million. Assume their home is now valued at $1 million and their mortgage loan has no lock-in period, which means they can now redeem their loan with no penalty.

Note:

The standard stamp duty is calculated as: 1% on the first $180,000, 2% on the next $180,000 and 3% for the remainder. A quicker way to calculate the stamp duty for properties $1 million and under is to take 3% of the property value minus $5,400. Find out more.

If the couple had bought the investment property without decoupling first, they will have to cough out an ABSD of 12% ($120,000) as it would be their second property.

If they decouple, their outlay includes the basic stamp duty of $9,600 (based on 50% of the property value) plus legal costs of about $7,500 amounting to $17,100.

The difference adds up to be more than $100,000!

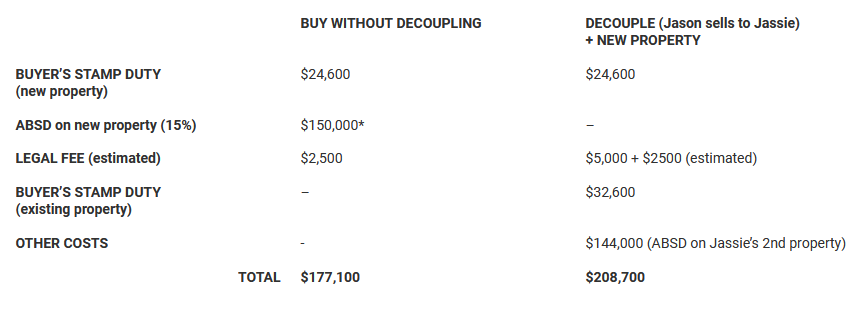

SCENARIO 2: WHEN THE SECOND PROPERTY YOU WISH TO BUY IS MUCH CHEAPER THAN THE CO-OWNED PROPERTY

Jason and Jassie co-own their residential property valued at $2.4 million as Joint Tenants (equal shares). They are keen to acquire an investment property for $1 million. Jassie owns another property in her own name many years ago before ABSD was implemented.

*The ABSD rate will be counted as third property for the couple because Jassie owns two properties.

Assume the couple opts to decouple and Jassie ‘buys’ over Jason’s share. There will be a standard stamp duty payable of $32,600. However, since Jassie owns another property here, she still has to pay ABSD of $144,000 (12% of $1.2 million) as this will be her second property.

On the other hand, if they opt not to decouple, their outlay will be lower. By not decoupling, it is more economical and the couple enjoys cost savings.

So the verdict in this case is not to decouple.

FINAL NOTE

How long does the decoupling process take for private properties?

It will usually take around 12 weeks for the decoupling process to take place. You may also be liable to pay for Seller’s Stamp Duty. You may refer to the IRAS website for more information.

Can the 2nd owner go ahead to purchase their 2nd private property while in the midst of the decoupling approval?

The second owner may go ahead to purchase their second private property while in the midst of the decoupling process.

If you need any assistance regarding decoupling or part-share transactions, please do not hesitate to contact Benjamin at (+65) 8778 8778 or Glynis at (+65) 8363 2331.

BUY WITHOUT DECOUPLING

DECOUPLE (Jason sells to Jassie)

+ NEW PROPERTY

BUYER’S STAMP DUTY

(new property)

$24,600

$24,600

ABSD on new property (15%)

$150,000*

–

LEGAL FEE (estimated)

$2,500

$5,000 + $2500 (estimated)

BUYER’S STAMP DUTY

(existing property)

–

$32,600

OTHER COSTS

–

$144,000 (ABSD on Jassie’s 2nd property)

TOTAL

$177,100

$208,700

We’re here to help you on your real estate journey.

Contact us using the form on this page and our Consultant will be in touch with you very soon.

Or contact us by phone/email.

Call: (+65) 8363 2331 / 8778 8778

WhatsApp: Glynis Tan / Benjamin Yeo

Email: findout@property-science.com