Decoding Real Estate

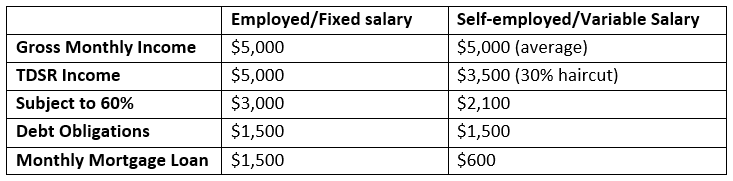

- If you have a fixed income, it is 100% of your monthly income.

- If you have a variable income (such as commission, bonus, overtime pay), only 70% is considered. There is a 30% ‘haircut’ factored in.

- Financial assets such as fixed deposit that are pledged with the bank for 4 years

Below is an example of how the TDSR works: