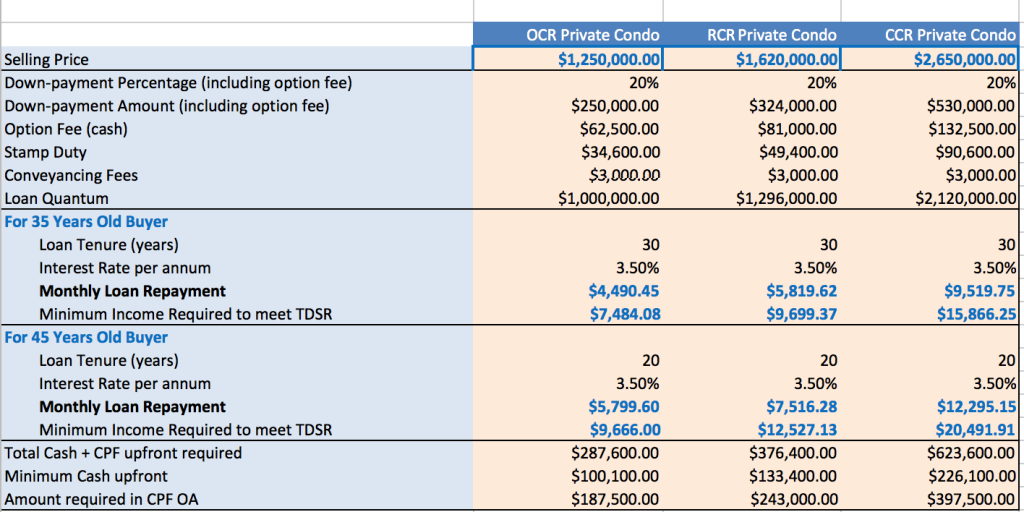

In this example, we assume the buyers are going for a bank loan instead of a HDB concessionary loan of 90%. The interest rate at 3.5% is a ‘stress test’ banks use to assess the loan quantum. Current rates hover at about 1.8% to 2% so your monthly repayment will be lower than those in the examples.

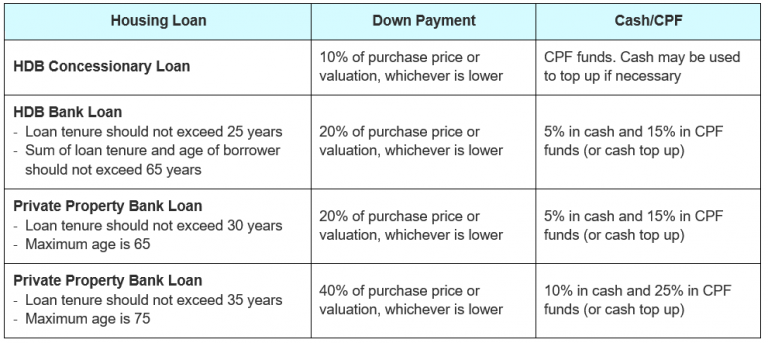

For HDB, the typical option fee is $1000 (although it can be less). In order to exercise the OTP, the buyer can pay up to a maximum of $5000, (inclusive of option fee), to the seller. We assume the figures are $1000 and $4000 respectively. Therefore, the initial Payment is the compulsory 5% cash component after payment of the Option Fee and Option Exercise Fee.

The Minimum Cash Upfront is assuming that you choose to pay your Conveyancing Fee and Stamp Duty on top of the 5% cash component by cash (although it can be paid with the CPF if sufficient). The Amount Required in CPF OA therefore is the remaining down payment of 15%. The Number of Years required portion gives one an estimate as to how long one needs to accumulate that 15% in the CPF OA.

In this example, we have used a double income totaling to at least $8400. If there are two borrowers for the property loan, we will use an Income Weighted Average Age formula to derive the final monthly loan figure.

The option fee is 5% of the purchase price, paid in cash. For Executive Condo (EC), we have to use HDB’s Mortgage Servicing Ratio of 30% to calculate loan size. Private condos and landed properties will be subject to Total Debt Servicing Ratio of 60% instead.

The Minimum Cash Upfront is assuming that you choose to pay your Conveyancing Fee and Stamp Duty on top of the 5% cash component by cash (although it can be paid with the CPF if sufficient). The Amount Required in CPF OA therefore is the remaining down payment of 15%. The Number of Years required portion gives one an estimate as to how long one needs to accumulate that 15% in the CPF OA.

In this example, we illustrate the costs and income needed for a 2 bedder 900sf condominium in either the Core Central Region (CCR), Rest of Central Region (RCR) and Outside Central Region (OCR). Prices are based on the time of this article, for a newly-TOP unit.

The interest rate is kept at 3.5% although current rates hover at about 1.8% to 2% so your monthly repayment will be lower than those in the examples.